EA Overview

| Logic Overview | Machine Learning |

|---|---|

| Martingale | No |

| Grid | No |

| Scalping | No |

| Trading Pairs | XAUUSD |

| Timeframes | 15M |

Forward Test Analysis

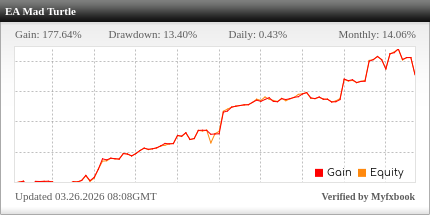

Forward Test Overview (as of November 21, 2025)

The forward test of this EA has been running on a real account (leverage 1:500) since the end of July 2025, and as of this writing, it is showing returns above the initial capital. The growth rate is roughly at a level of more than +100%, while the maximum drawdown is held to less than 10%. This suggests that, although the design leans toward aggressive trading, it is not the type of EA that blows up the account in a single hit.

Evaluation of Risk–Reward and Win Rate

Looking at the quality of the risk–return profile, the profit factor is around 2, and the win rate is close to 70%, indicating a certain degree of statistical edge. On the other hand, the average loss per trade is almost the same as the average profit, so the risk–reward ratio is slightly below 1. In other words, this is not an EA that “earns a lot of pips per trade”; rather, it appears to be a logic that builds positive expectancy by holding many positions simultaneously and combining that with a somewhat higher win rate.

Trading Style and Market Suitability

Although the forward period is still short, the total number of trades has already exceeded 1,000, which is due to the EA often holding many positions at the same time. Breaking the trades down further, we see a strong bias toward long positions, with only a very small number of shorts. From this, we can infer that the EA is primarily designed to perform well in rising trends or markets where buying has an advantage, and that its edge on the short side is likely limited. In live trading, special attention should be paid to how it behaves when the overall market transitions into a significant downtrend.

Summary and Future Points of Caution

The equity curve, while experiencing dips and consolidation phases along the way, is overall trending upward, indicating that the logic has functioned well under the market conditions observed up to the time of writing. However, the verification period is still only a few months, and there is no guarantee that the performance seen so far can be reproduced over the long term. It will be important to continue the forward test and, by evaluating at least one year of live data as well as results from different brokers, avoid excessive expectations and more accurately gauge the EA’s true capabilities.

Backtest Result Analysis

Backtest Conditions and Period

In this section, I summarize the EA’s long-term behavior based on the backtest results I personally ran using the MT5 Strategy Tester. The main backtest conditions are as follows:

- Period: January 1, 2005 – November 15, 2025 (approximately 20 years of data)

- Symbol: XAUUSD (gold)

- Lot size: fixed 0.01 lots

- Spread: fixed 60 points

- Initial deposit: USD 10,000

- History quality: 98%

The test covers more than 20 years, with a total of 4,159 trades and 8,318 deals, providing a statistically meaningful sample size.

Equity Curve and Drawdown

The equity curve shows a period of prolonged stagnation and floating drawdowns in the first half of the backtest, followed by a gradual recovery and an increasingly steep upward slope in the latter half. The final account balance reaches about USD 13,188, indicating that the EA steadily built equity over the long term.

In terms of drawdown, the maximum equity drawdown is around USD 558, which is relatively moderate, corresponding to roughly 5.5% of the initial USD 10,000 deposit. So, while this is not an EA that “loses a large portion of capital in a single blow,” the equity curve also shows that there are multi-year periods during which the account is stuck in drawdown or stagnation. In other words, this is a strategy whose risk manifests more as the length of time spent underwater rather than as the magnitude of the loss in monetary terms.

Evaluation of Statistical Metrics (Win Rate, PF, Expectancy)

Over the full backtest, the total net profit is approximately USD 3,188, with a profit factor of 1.21. The win rate is about 55% (2,278 profit trades vs. 1,881 loss trades). The average profit is around USD 8.19, and the average loss is -USD 8.22, so the per-trade profit/loss span is almost symmetrical. With a fixed lot size of 0.01, the expected payoff is about USD 0.77 per trade, which clearly shows that this is not an EA designed for explosive growth but one built to accumulate a very small edge over the long term.

At the same time, looking at the trade breakdown, we find that there are zero short trades and that all entries are long positions. This long-only structure is also confirmed in the forward test. It means the logic is heavily dependent on the long-term bullish bias of gold, and that the backtest results are based on the assumption of the rising trend over the past 20 years. If gold were to enter a prolonged downtrend in the future, there is no guarantee that the same results could be achieved.

Strengths and Cautions Seen in the Backtest

The strengths visible in this backtest, under the assumption of a fixed 0.01 lot size, include:

- The maximum drawdown is generally limited to a few hundred dollars.

- Over about 20 years, net profit of just over USD 3,000 has been accumulated.

Under the assumption of operating with a modest 0.01 lot size, the equity curve is relatively smooth, and we can say that the risk of account blow-up is kept low.

On the other hand, the weaknesses and points of caution include:

- The strategy is long-only and has no edge on the short side at all.

- The net profit of approximately USD 3,188 over 20 years means that the return per unit time is not particularly high.

- There are multi-year periods during which the equity barely grows (in the backtest, the 2005–2014 period is spent largely in drawdown).

In particular, the fact that this is a one-sided strategy biased toward buying greatly affects how we should interpret these backtest results. Given that the long-term uptrend in gold has likely been a significant tailwind, it is important to evaluate the strategy cautiously, recognizing that similar conditions may not continue indefinitely.

Rather than blindly trusting the backtest numbers, it is crucial to clearly define lot-sizing rules and stop-trading thresholds while taking into account forward test results, the current market environment, and potential structural changes in the gold market.

Trading Logic and Risk Characteristics

Assumptions as a Machine-Learning EA and the Developer’s Concept

According to the developer’s official page (the product description on the MQL5 Market), this EA employs a machine-learning-based logic. It is designed to learn patterns from historical data and to enter only in situations where there is a statistically significant edge. At the same time, as is always the case with machine-learning EAs, the risk of over-optimization (overfitting) should never be overlooked. Even if the backtest shows a beautiful curve, there is no guarantee that the same results will be reproduced in forward testing.

As indicated by the forward test discussed earlier, we can confirm that the logic has functioned well in the real environment so far. However, this is merely a snapshot of a period during which things have gone well. It remains important to keep monitoring forward behavior on an ongoing basis.

Trading Tendencies Observed from the Trade History Chart

Looking at the trade history chart, we can see that this EA has a relatively high trading frequency and that once a signal appears, it tends to stack multiple positions in a step-like fashion. There are many situations where white markers (buys) line up in sequence, with red markers (sells) interspersed at certain points, and overall, it is clear that long positions are the main focus.

A bird’s-eye view of the forward history shows that, especially during the recent uptrend in gold, the EA has been splitting entries into small positions along the uptrend and capturing profits in a trend-following manner. At the same time, in phases where the chart is dropping sharply, we see very few new entries, giving the impression that the EA is successfully avoiding those drops.

As shown in the image below, some trades exhibit behavior reminiscent of a grid EA. Positions are opened in stages and then closed collectively. However, at least so far, there have been no situations where positions are simply held and waited on indefinitely until the market returns. At this point, it is reasonable to interpret this EA as not being a dangerous, contrarian martingale that stubbornly holds losing positions.

Risk Profile and Dependence on Market Conditions

From both the backtest and forward-test statistics, we see that the average profit and average loss are nearly identical, so the per-position risk–reward ratio is not particularly skewed. This means that, at the level of individual trades, the EA is not taking excessively large risk.

However, the actual trade history shows a strong tendency to stack multiple positions in the same direction once trading starts, so it is important to consider “how much risk is being taken in total for each signal.” With small lot sizes, this may not be a major issue, but if you increase the account size or the lot size, you must implement risk management based on total position exposure (such as setting upper limits on the number of positions and total lot size).

Moreover, since the EA’s logic is structurally biased toward long trades, it cannot be denied that part of its success in the forward test has come from “simply riding the uptrend in gold.” If gold were to enter a long-term downtrend, it is unclear whether the strategy could maintain the same level of performance. It is therefore reasonable to view this EA as one that depends significantly on the prevailing market environment.

Current Evaluation and Future Verification Points

In recent forward tests, when gold experienced a sharp drop, the EA largely refrained from opening new trades, which is highly commendable behavior in that it appears to avoid dangerous countertrend entries. If this is not merely coincidental but part of a logic designed to “avoid taking risk during strong countertrend moves,” it would be a major strength of this EA.

That said, the forward sample period is still shallow, and we cannot completely rule out the possibility that it is simply benefiting from a period of favorable uptrend conditions. At this point, the fairest stance seems to be that both the past backtest and the recent forward test indicate some degree of edge, but the long-term reproducibility remains to be seen.

If you are considering running this EA, it would be wise to:

- Continue forward testing with small lot sizes and accumulate at least one year of real trading data.

- Pay particular attention to how it behaves during phases when gold undergoes large corrections or declines.

- Define in advance risk-management rules based on total position exposure, including maximum total lots and maximum number of open positions.

Taking these points as prerequisites will help you evaluate this EA’s trading logic and risk characteristics more fairly.

Overall Evaluation and Practical Considerations for Live Trading

- Both backtest and forward-test results indicate a positive expected value.

- The per-trade profit/loss span is not extremely high-risk, as average profit and average loss per trade are nearly identical. However, because the EA stacks multiple positions in the same direction when a signal occurs, risk management at the level of the entire trade set (maximum number of positions and upper limits on total lot size) is essential.

- In the forward test, the EA has generated large profits by simply riding the uptrend in gold. At the same time, its long-biased logic means that its resilience to long-term downtrends or structural shifts in the market has not yet been sufficiently tested.

- In the long-term backtest from 2005 to 2025, the maximum drawdown was kept within a range of a few hundred dollars, and with a 0.01 lot size, the equity curve is relatively smooth. However, the net profit of just over USD 3,000 also means that the return per unit time is not particularly high, which should be clearly understood in advance.

- As of around November 2025, the sale price is roughly around USD 1,200, placing it in the very expensive category for an EA. If you soberly compare the expected long-term average return to this price, you will find that a certain length of time and a sufficiently large account size are required to recoup the investment. Until ample forward results are accumulated, it is realistic to remain cautious and observe rather than rushing to commit heavily.

This EA does not use martingale or unlimited grid strategies, and the average loss per position is kept roughly on par with the average profit, so the risk of each individual trade is not extremely large. On the other hand, when a signal occurs, it tends to stack multiple positions in the same direction in a step-like manner, so total position size can easily expand. Extra caution is required if you plan to run it with larger lot sizes.

According to the developer, this EA uses machine learning algorithms to extract statistically advantageous patterns and implements a trend-following logic that mainly takes long positions. In recent forward tests, we can observe risk-avoiding behavior, such as refraining from opening new trades during strong downtrends. However, the strategy is structurally biased toward long positions and undeniably depends on the long-term bullish bias of gold. It is still unknown how well it can cope with a prolonged downtrend or structural changes in the market.