When running an EA, what matters most in the end?

Win rate? PF (Profit Factor)?

What matters most isn’t flashy numbers—it’s robustness (how hard it is to break).

What Is EA Robustness? A Beginner-Friendly Explanation

Robustness means, in simple terms, “staying strong even when conditions change.”

An EA’s performance can change depending on many factors: market conditions (trend/range/volatility), spread, slippage, execution quality, trading hours, and more. A robust EA tends to avoid sudden blow-ups or performance collapsing to zero, even when these conditions shift.

Related article: What Is an EA? How FX Auto-Trading Works and How to Choose One | Complete EA Guide

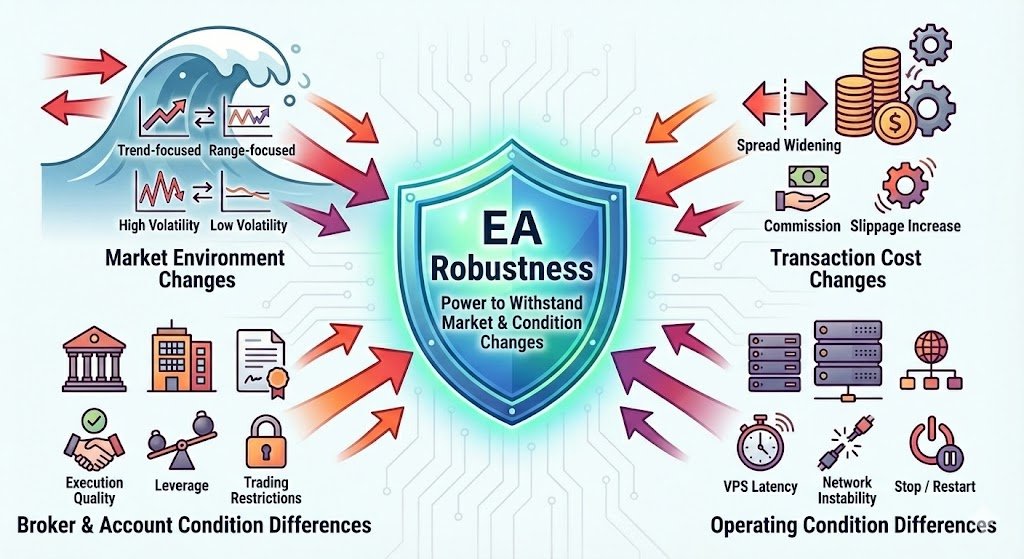

Robustness = “The ability to avoid breaking when markets and conditions change”

It’s easier to picture robustness as the ability to handle these kinds of “changes”:

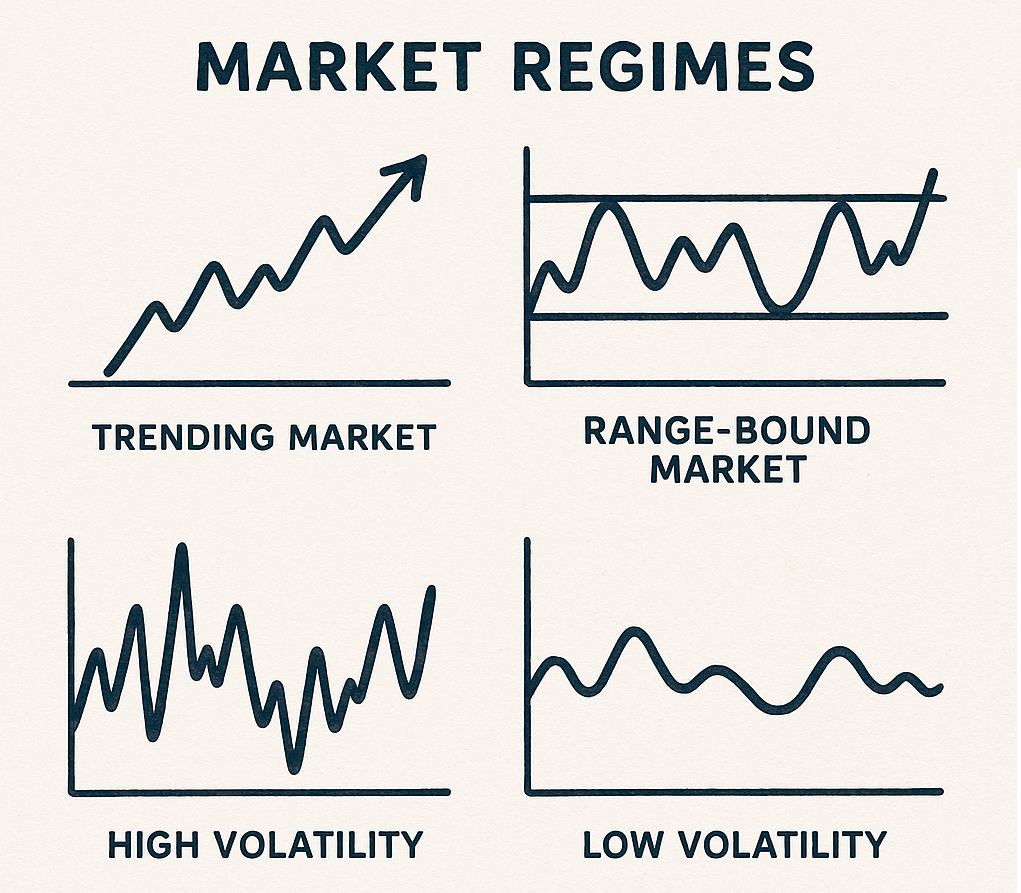

- Market regime changes: trend-heavy → range-heavy, volatility spikes → volatility drops, etc.

- Trading cost changes: wider spreads, commissions, more slippage

- Broker/account differences: execution quality, leverage, trading restrictions

- Operational differences: VPS latency, connection issues, stops/restarts

In other words, a robust EA isn’t just “great under a short period or one special condition.” It’s more likely to avoid taking fatal damage when the market or environment changes.

Robustness does NOT mean “always winning” (how it loses matters)

A common beginner misunderstanding is thinking robustness means “an EA that keeps winning with a smooth upward curve.” That’s not reality.

What truly matters in robustness is not how it wins, but how it loses.

- Bad example: wins most of the time, but occasionally gives back all profits in one hit (small wins, big blow-up)

- Bad example: holds losing positions for a long time, then takes one large loss (Equity sinks in an unnatural way)

- Good example: even during losing periods, losses are controlled and less likely to become fatal

In long-term trading, avoiding a major collapse is more valuable than short-term flashy performance. Because with EA trading, one account wipeout ends the game.

Difference from over-optimization: robustness is a “total evaluation axis”

One of the biggest dangers in EA trading is over-optimization (overfitting)—tuning the EA too tightly to past data so it falls apart in live trading.

Related article: What Is EA Over-Optimization (Overfitting)? How to Spot It + Pre-Purchase Checklist

Robustness goes beyond just avoiding overfitting. It’s a broader, overall framework for evaluating an EA.

- Overfitting: mainly caused by how the backtest was built and excessive tuning

- Robustness: checks “how hard it is to break,” including market changes, costs, execution, and operational conditions

So robustness includes avoiding overfitting, but goes one step further: “Will this EA survive in future conditions?”

From a buyer’s point of view, rather than focusing on pretty backtest numbers, it’s safer to judge an EA using a mix of forward performance, how it loses, cost tolerance, and how stable it stays when conditions change.

Why Robustness Matters: 6 Common Reasons EAs Break in Live Trading

When choosing an EA, many people start with backtest stats (PF, win rate, DD, etc.). Those matter—but the real long-term difference comes from robustness (how hard it is to break).

An EA can fail for many reasons. Below are six typical causes, explained in a beginner-friendly way.

Cause 1: Over-optimization (tuned too tightly to the past)

Overfitting happens when an EA is tuned too closely to past data, so it stops working in future markets.

- Backtest looks “too perfect” (win rate/PF unrealistically high, DD unrealistically low)

- In forward trading, PF suddenly drops and DD increases

More robust EAs rely less on one specific slice of history and tend to degrade more gently when conditions change.

Cause 2: Low resistance to market regime changes

Markets never stay the same. Trending markets and ranging markets rotate, and volatility changes over time.

This is often called a “regime change.”

If an EA performs only in its favorite market and collapses in its weak market, it won’t survive long-term.

- A trend-following EA keeps losing in a range market

- A mean-reversion EA takes big losses in a strong trend

- A low-volatility EA suffers unexpected losses when volatility suddenly spikes

You must check whether a weak market period can continue without becoming fatal.

Cause 3: The “small wins, big blow-up” structure (poor risk-reward)

Even if an EA has a high win rate and looks great, it can be dangerous if the average loss is larger than the average win (low RR).

- It stacks small profits

- Then occasionally takes a large loss and gives back the gains at once

This type often looks attractive in backtests or short-term forward results, but performance can break badly over time.

More robust EAs tend to be designed so that one trade loss is less likely to be destructive.

Cause 4: One-hit knockout (grid / martingale)

Grid (averaging down) and martingale strategies can look “hard to lose” in the short run.

But when price moves against the position for a long time, losses can explode, with a risk of heavy account damage—or even total wipeout.

- Even if the Balance curve looks smooth, Equity can sink deeply from floating loss

- The more it “holds and waits for a comeback,” the higher the risk of failure

From a robustness standpoint, any structure that can cause a one-hit knockout is a potentially fatal weakness by itself.

Related articles:

Don’t Get Fooled by Martingale EAs: How They Blow Up Accounts and How to Spot Them (Tested)

Don’t Get Fooled by Grid (Averaging-Down) EAs: Account Blow-Up Risk and How to Spot It (Tested with a Self-Made EA)

Cause 5: Low tolerance to trading costs (spread, commission, slippage)

The shorter the trading style (especially scalping), the more trading costs matter. Even if the backtest looks good, weak assumptions can make live results collapse easily.

- Assumes an unrealistically tight or fixed spread

- Doesn’t include commissions

- Assumes zero slippage

Robust EAs tend to be less likely to die instantly even if costs get slightly worse (profits may shrink, but it’s less likely to break).

Related article: Can Scalping EAs Really Win? Why I Don’t Recommend Them (Watch Out for Low Reproducibility)

Cause 6: Operational issues (VPS stops, connection drops, restarts)

A surprisingly common blind spot is “operational weakness.” If the program stops, trading stops.

- VPS freeze/stop leads to missed exits and larger losses

- Connection drops delay orders and cause worse fills (slippage)

- After restarts, unexpected duplicate orders or broken management logic can occur

More robust EAs often have SL/TP set on each position and are designed so that even if trading stops, it’s less likely to become fatal (for example, relying more on pending orders/stop orders).

Summary: Robustness matters not only “to win,” but to survive and avoid fatal damage. The more you feel drawn to flashy short-term numbers, the more you should first suspect weaknesses in one of these six areas. That’s one of the safest mindsets buyers can have.

Traits of a Robust EA: Focus on “How It Loses,” Not “How It Wins”

A robust EA isn’t designed to produce explosive short-term profit. It’s designed to be hard to break and more likely to survive long-term.

So as a buyer, you should pay more attention to how it loses than how much it wins. The less destructive its losses are, the more likely your capital survives—giving you a better chance of growth over time.

Instead of win rate, look for healthy RR (avg win ÷ avg loss) and max loss

Many beginners assume “high win rate = good EA.” In reality, even with a high win rate, a low risk-reward ratio can still lead to one big loss wiping out profits.

- RR (average win ÷ average loss) is not extremely low

- Check whether the maximum loss is “how many times the average win” (this is the most important)

- After a winning streak, it doesn’t lose most gains in one trade

More robust EAs can have a lower win rate, but they tend to lose in ways that are less likely to be fatal.

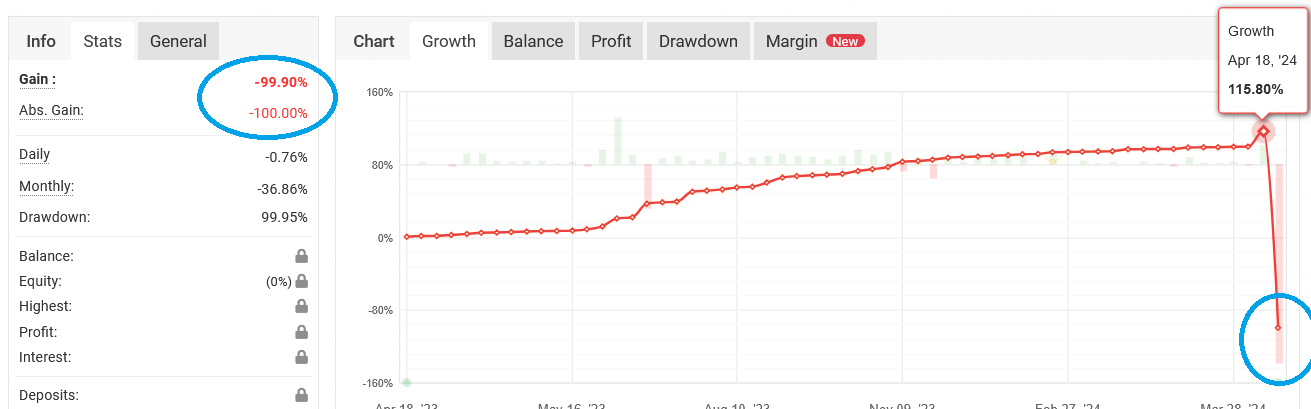

Small gap between Equity and Balance (doesn’t “survive on floating loss”)

When evaluating an EA, always look at Equity, not just Balance. If the gap is large, it often means the EA holds large floating losses, making the real risk hard to see.

- Equity doesn’t stay deeply underwater for long periods

- Even if Balance looks smooth, Equity isn’t collapsing

- It’s not built on the assumption of “hold until it comes back”

Robust EAs tend not to “kick the can down the road” by sitting on floating losses. They bring risk to the surface and manage it.

Note: MT5 backtest reports in HTML format do not reflect Equity changes.

Also, the Equity curve on Myfxbook is helpful, but it’s a “snapshot” based on update timing. Sharp drops that happen between updates (max floating loss / instant DD) can be missed, making risk look smaller than it really is. When you evaluate an EA, also check trade history (how it loses, max loss, lot size changes) and whether SL/TP is used. Even if the Equity curve looks fine, there may still be large hidden Equity drawdowns.

Designed to avoid “one-hit losses” (stop-loss, lot sizing, averaging-down behavior)

The scariest long-term risk is a loss that ends the game in one hit. Robust EAs are designed so a one-hit loss is less likely—or even if it happens, it’s less likely to be fatal.

- Each position has an SL (stop-loss), so losses are capped

- It does not use averaging down (grid) or martingale

The core of robustness is not “easy to win,” but “hard to die even when it loses.”

Not overly condition-dependent; more general (not limited to one time, year, or single pair)

More robust EAs are usually less dependent on narrow conditions.

On the other hand, the narrower the conditions, the easier it is to “break the moment that condition changes.”

- Not “absurdly strong in one specific year (and weak elsewhere)”

- Not profitable only in one specific time window or weekday

- Not “one pair is great while everything else is a disaster”

A “specialized strategy” isn’t always bad. But as a buyer, you should understand that the narrower the conditions, the easier it is for reproducibility to drop.

Doesn’t collapse easily even if costs get slightly worse

In real trading, spread, slippage, and commissions are not always stable. Robust EAs tend to avoid sudden performance collapse even when costs become slightly unfavorable.

- PF doesn’t collapse just because the spread widens a little

- Slippage doesn’t easily become fatal

- It’s not a strategy that only works under ultra-low-cost assumptions

Scalping EAs are especially cost-sensitive. Before buying, check whether the EA can realistically reproduce results with the broker and account type you plan to use.

Summary: A robust EA isn’t one that “keeps winning forever.” It’s one where losses aren’t destructive and it can survive even when the environment changes. Before you get impressed by big numbers, check how DD grows, RR and max loss, the Equity vs Balance relationship, and whether one-hit losses exist.

How to Judge Robustness: 6 Checks to Do Before Buying an EA

You can’t judge robustness from marketing alone. As a buyer, the realistic approach is to use public data and what you can verify yourself to assess “how hard it is to break.”

Here are six key checks that beginners can follow without getting lost. You don’t have to do all of them—but if even one check raises a serious red flag, don’t rush the purchase.

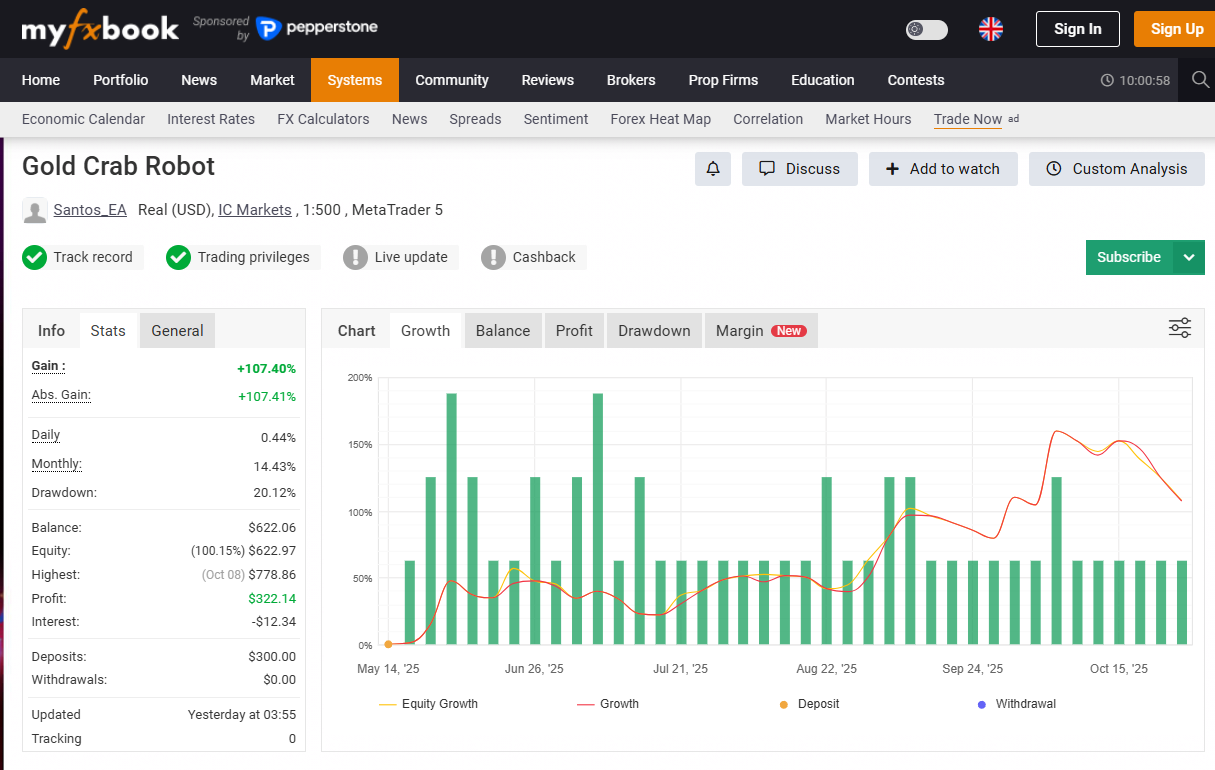

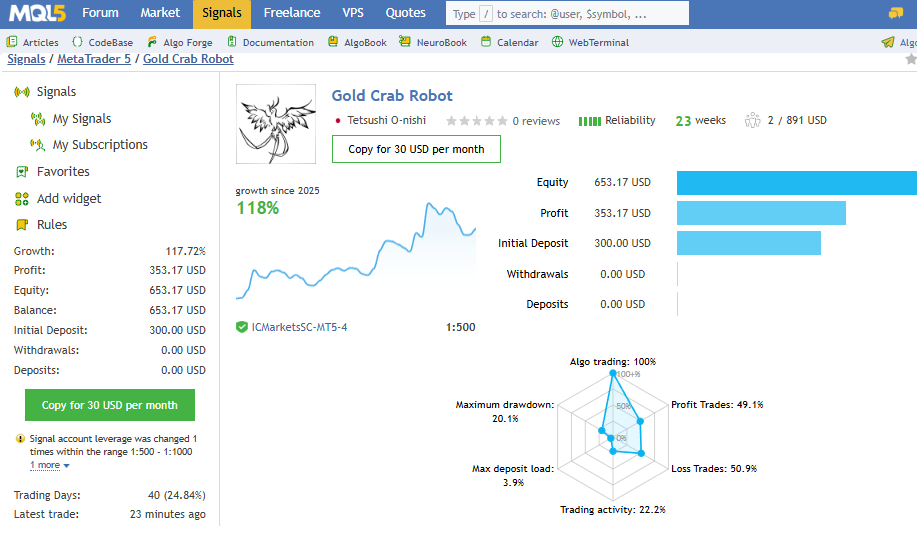

Check 1: Is there forward performance (ideally on a real account)?

The top priority for checking robustness is forward performance (live trading record).

It’s relatively easy to make a good-looking backtest, but forward performance is harder to fake.

- Is performance continuously published on Myfxbook / MQL5 Signals, etc.?

- Is it a real account? (Demo results are only参考. Some EAs look great on demo but fail on real accounts.)

- Are key assumptions clearly stated (broker, account type, commissions, etc.)?

- Is it more than just short-term good results?

Key point: If there’s no forward record (or proof is weak), it’s “not enough data” even before robustness.

Also, never assume “forward record is public = safe.” An EA with small wins and rare big losses can look excellent in short-term forward results due to a high win rate—until the day it takes a huge loss. Always review trade history along with the curve to understand the trading behavior.

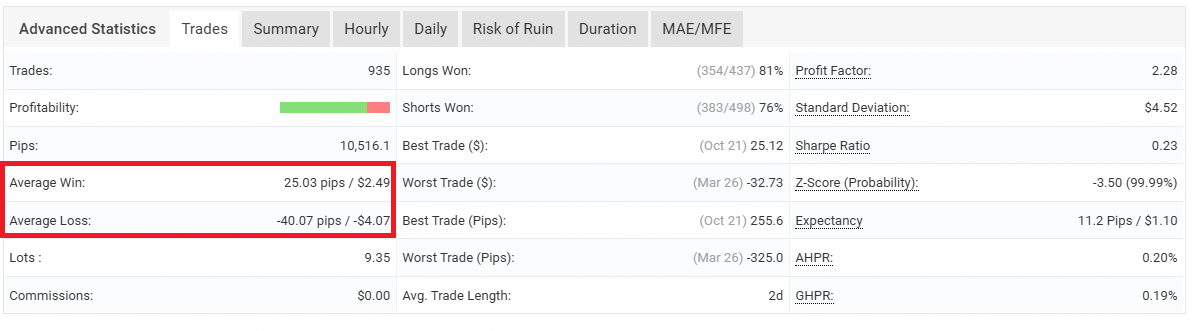

Check 2: Confirm “how it loses” in the trade history (RR, max loss, SL/TP)

Robust EAs don’t lose in a destructive way. Don’t judge only by return percentage or a profit curve—always review basic stats and the trade history.

- Is RR (average win ÷ average loss) not extremely low?

- Is the maximum loss multiple times larger than the average win? (This is the biggest landmine.)

- Does each position have SL (stop-loss) / TP (take-profit)? (“Basically no SL” is a major warning.)

- Does lot size jump sharply after losses (a sign of martingale behavior)?

Key point: High win rate + low RR + abnormally large max loss is a classic pattern that breaks over the long run.

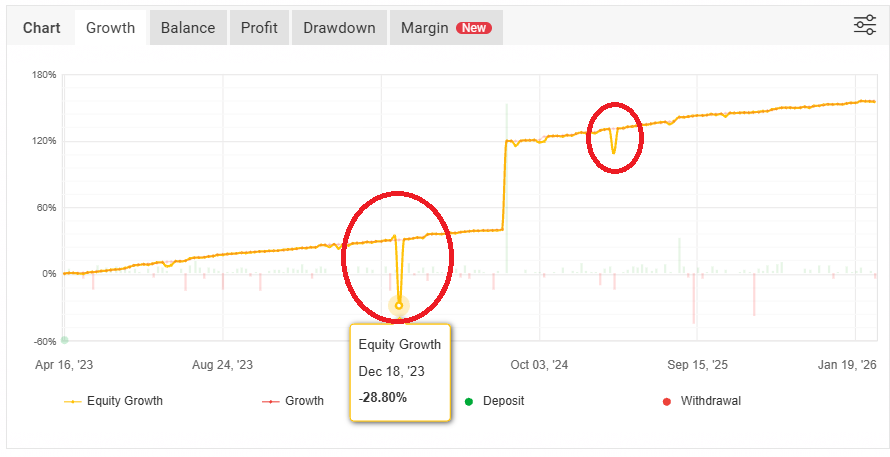

Check 3: The gap between Equity and Balance (spot floating-loss strategies)

Even if the Balance curve looks like a smooth upward line, be careful if Equity sinks deeply.

This often means the EA delays cutting losses and “endures” until the position turns profitable.

With a floating-loss structure, risk can be larger than it looks.

- Does the Equity–Balance gap become large frequently?

- Does Equity stay deeply underwater for a long time (long “endurance time”)?

- Is it built on “hold until it comes back” instead of cutting losses?

Key point: Robustness is not about a “beautiful Balance curve.” It’s about whether the EA avoids fatal damage even through drawdowns and flat periods.

Check 4: Test duration and number of trades (avoid small samples)

You can’t judge robustness from a short period. Markets cycle through regimes (trend, range, high vol, low vol, etc.), so you need to see whether the EA survives across different environments.

- Is the period not too short? (For backtests, 20+ years is recommended.)

- Is the number of trades not too low? (500+ trades for backtests; ideally 1,000+.)

- Think in terms of trades per strategy logic, not just total trades (packing many logics into one EA can increase overfitting risk)

Key point: Longer periods and more trades generally increase reliability in both backtests and forward tests.

Check 5: Does it avoid blowing up on other currency pairs (if possible)?

If you can, test the same settings on other pairs—not to chase bigger profits, but to check whether it avoids blowing up. EAs with strong overfitting or condition dependence tend to break under different conditions.

- It collapses instantly on another pair → may be highly condition-dependent

- It “loses in similar, controlled ways” across multiple pairs → logic may be stable

- Can’t run/test on other pairs → a reason to lower purchase priority

Key point: It’s less about “can it make money on other pairs” and more about “does it avoid a major collapse.”

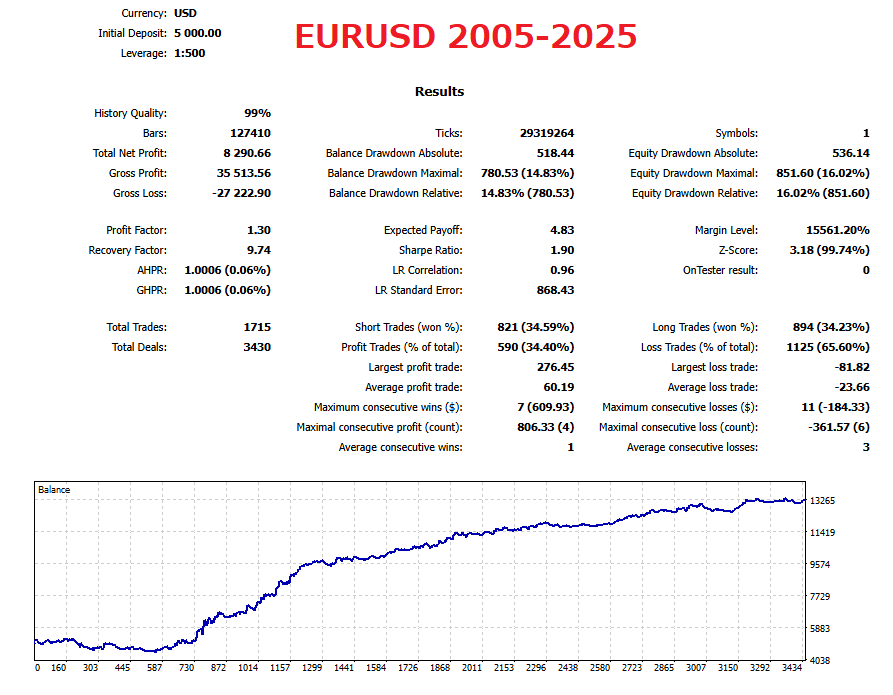

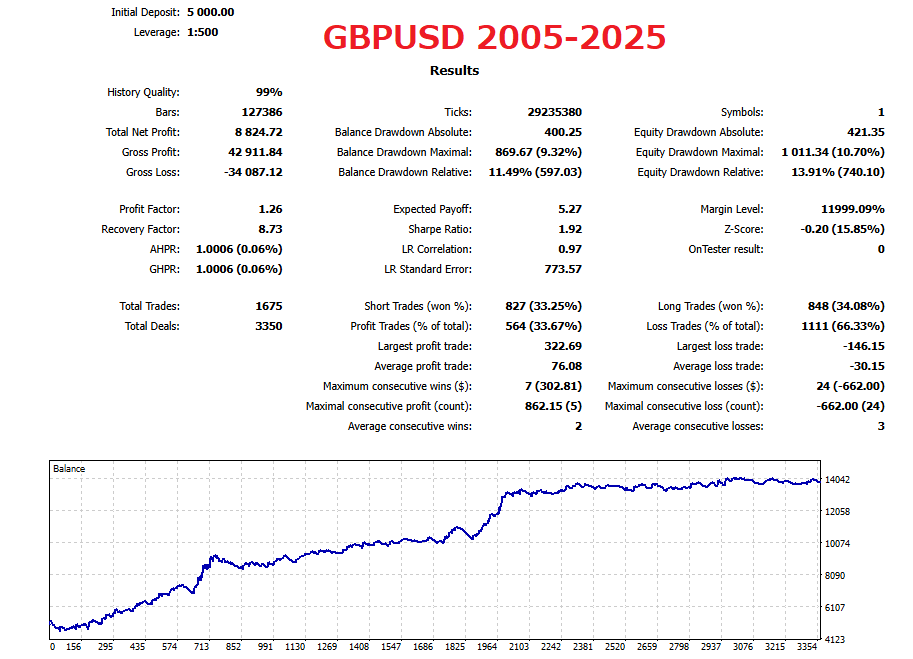

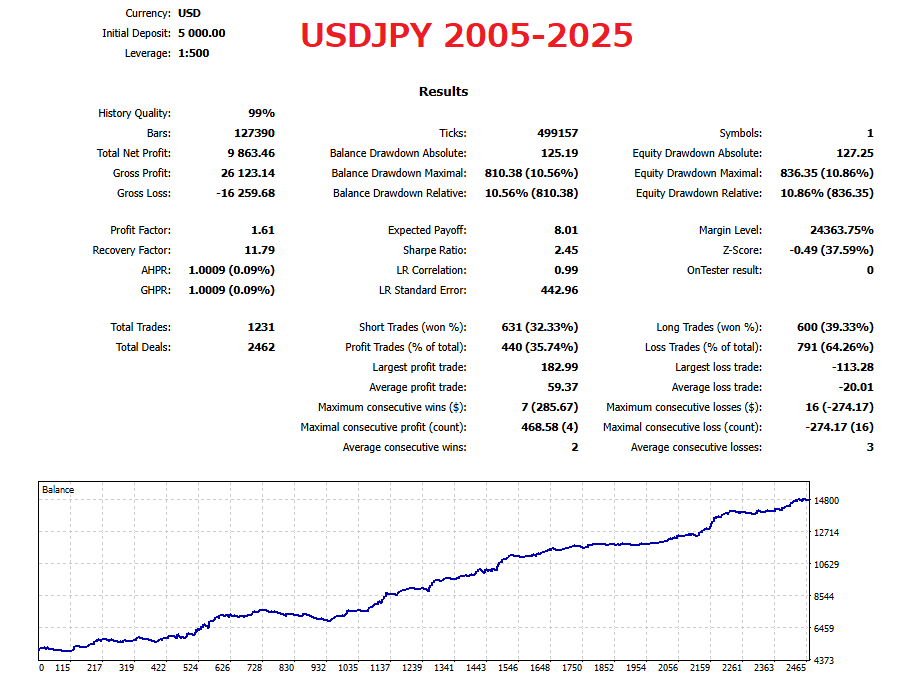

Below are the results of a multi-currency backtest for my own EA, Colorful Long tailed Tit EA.

The test period is 20 years, from 2005 to 2025.

Check 6: Cost tolerance and operational risk (spread widening, VPS stops)

In live trading, results can worsen due to factors that are hard to test properly in backtests: spread widening, slippage, rejected orders, connection drops, etc.

Robust EAs tend not to degrade dramatically even under these real-world conditions.

- Does performance avoid collapsing when the spread gets slightly worse? (especially important for scalping EAs)

- Does it assume slippage during news and low-liquidity hours?

- Even if VPS/PC stops or MT5 stops, is it designed so SL/TP (server-side stop orders) still work?

- Is it dangerous if “the EA isn’t running” (stop-loss depends on EA-side logic)?

Key point: You’ll judge robustness more accurately when you include not only “market risk,” but also “operational trouble.”

Operational Robustness: EAs Can Lose Due to “Environment Problems,” Too

When people talk about EA robustness, they often focus only on logic and backtest results.

But in reality, if your trading environment (infrastructure) is unstable, unexpected losses can happen.

Even the best strategy can suffer “avoidable losses” when server downtime, disconnections, power issues, or PC restarts hit at the wrong time.

This section explains how to strengthen operational robustness through VPS/PC, network, and power risk management.

Operational robustness = resisting both “market changes” and “environment changes”

Operational robustness means an EA can handle not only market changes, but also operational risks (stops, delays, disconnections).

- Even with great logic, an unstable environment can cause missed entries and late stop-outs.

- Especially for EAs that require 24/5 operation, uptime reliability directly affects performance.

Think “VPS-first” for 24/5 operation: eliminate weak points of PC trading

For EAs that must run continuously, a VPS is the standard.

A home PC has many reasons to stop—power outages, network issues, Windows updates, restarts—making it a long-term disadvantage.

- VPS benefits: less affected by power issues; better suited for 24/5 operation

- PC risks: auto-updates, sleep mode, power-saving settings can stop trading

- Minimum steps: disable sleep; reduce/avoid forced updates and restarts

The goal is to build an environment where the EA doesn’t stop.

Latency reveals a strategy’s weak points: prioritize durability over speed

Scalping strategies are generally more sensitive to latency (execution delay) and spread changes.

From a buyer’s perspective, it’s often safer to choose a strategy that doesn’t break even with some delay, rather than trying to create the fastest possible setup.

- The more an EA needs latency optimization, the more results vary across environments

- Rather than “it wins only in a fast environment,” it’s better if it stays stable in a normal environment for long-term use

Most important: protect yourself with broker-side orders like SL/TP

This is the single most important point for operational robustness.

Even if the EA or MT5 stops, if you have stop orders (SL/TP) registered on the broker side, you are far more likely to avoid a worst-case accident.

- Likely to work even if the EA stops: SL (stop-loss) / TP (take-profit) and other orders stored on the broker server

- More dangerous when it stops: exits that depend on EA-side local logic (some conditional exits, some trailing/management logic)

- Pre-purchase check: Does each position “always” have SL/TP attached? (confirm in history and live screens)

Conclusion: You can’t reduce the chance of VPS/PC issues to zero. That’s why you should prioritize confirming order design that avoids fatal damage even if the EA stops (SL/TP).

Conclusion: “Boring but hard to break” EAs tend to win more often in the long run

To grow capital over the long term, what matters isn’t “flashy short-term results,” but robustness (how hard it is to break).

Markets change, costs worsen, and operational trouble happens.

EAs that survive in the real world are the ones that often end up growing balances over time.

What to check (in this priority order)

When evaluating EA robustness, check in this order:

- Forward performance (ideally real-account record): confirm “real results” exist

- How it loses (RR, max loss, SL/TP, Equity): check for hidden one-hit blow-up risk

- Cost tolerance: does it break under slightly worse conditions?

- Sample size (time period and trade count): don’t get fooled by short-term luck

(Warning) EAs to avoid: flashy short-term, one-hit losses, strong condition dependence

- Backtest or short-term forward results look too perfect (extreme win rate/PF, unrealistically tiny DD)

- Abnormally large max loss / extremely low RR (small wins, big blow-up)

- Large Equity–Balance gaps, often enduring floating losses

- Scalping EAs with very tight target ranges

- Overly narrow conditions like “only this broker, this pair, this timeframe” (low generality)

- Testing/history disclosure is vague or frequently becomes private

Re-check as much as you can on your own

Don’t rely only on the developer’s backtest and short-term forward results. Verify as much as possible yourself.

- Backtest with cost settings close to the broker conditions you plan to use

- Extend the backtest period to verify long-term durability

- Backtest on other currency pairs to see whether it avoids blowing up

- If using a VPS, confirm SL/TP design so stops/restarts don’t become fatal

Final takeaway: Don’t get distracted by flashy performance. Put “Does it break easily?” first.

That mindset significantly improves long-term survival—and results.