Can contrarian EAs really make money?

Bottom line: They can look easy to win with in the short run, but it’s hard to stay profitable consistently over the long run.

They tend to work in ranging markets, but performance can flip overnight when you hit a “no-pullback day” and take a big loss.

In this article, using test results from a sample EA, I’ll explain how to judge contrarian EAs based not on “win rate,” but on “how they lose” and whether the strategy is built to survive.

What Is a Contrarian EA? Key Traits and the Biggest Risk

A contrarian EA (also called a mean-reversion or counter-trend EA) is an automated FX strategy that targets short-term “overshoots,” betting that price will calm down and drift back toward its average.

In range-bound markets, or during short-lived pullbacks, these systems can stack small gains steadily. But if the design is weak, they also carry the risk of blowing up in a single session when price simply doesn’t come back.

Related article: What Is an EA? How Forex Trading Bots Work and How to Choose One (Complete Guide)

By nature, contrarian strategies often require patience while waiting for the reversal. That structure tends to produce small wins and big losses (high win rate, poor payoff).

During a winning streak, results can look great. But when a trend keeps extending (driven by news, central bank policy, geopolitics, flash crashes, etc.), floating losses can grow quickly, and you can give back profits and see performance collapse. That’s not rare.

That’s why you shouldn’t judge a contrarian EA by win rate or a nicely rising equity curve alone. Over the long run, you should prioritize how it loses and its survival design (risk management).

In this article, based on tests with a sample EA I built (optimization distribution and backtest summaries), I’ll break down the limits of contrarian logic by itself—and why filters and exit design often decide whether results hold up.

Contrarian EA Basics: The Core Idea and Common Logic

The Concept

Contrarian EAs look for the moment when a heated move starts to cool off, then trade the move back toward the mean (the “center”).

- They aim to catch reversals after short-term overbought/oversold conditions

- They also try to capture the “snap-back” after an overreaction (often right after major news)

Typical Logic Examples

Common implementations include:

- A reversal after RSI reaches an extreme level

- A reversal after price touches the Bollinger Bands ±2σ line

- A reversal after price deviates far from a moving average

- A reversal after price hits the prior day’s high/low

Case Study: Testing 3 Self-Built Sample EAs (Backtest & Optimization)

Here, I built three sample contrarian EAs myself and tested them using backtests and parameter optimization.

For patterns (1) and (2), I used the 1-hour chart (H1) over 20 years to check long-term durability. For pattern (3), I tested a contrarian scalping approach on the 5-minute chart (M5) over 5 years.

For each one, I organized:

optimization distribution (parameter sensitivity), backtest summaries, and key observations.

If I summarize the conclusion upfront: contrarian entry logic alone often struggles to produce a strong edge, and performance is heavily determined by the filters you add.

What matters most isn’t “how to win,” but how you avoid the blow-up conditions—and how you keep losses small when things go wrong.

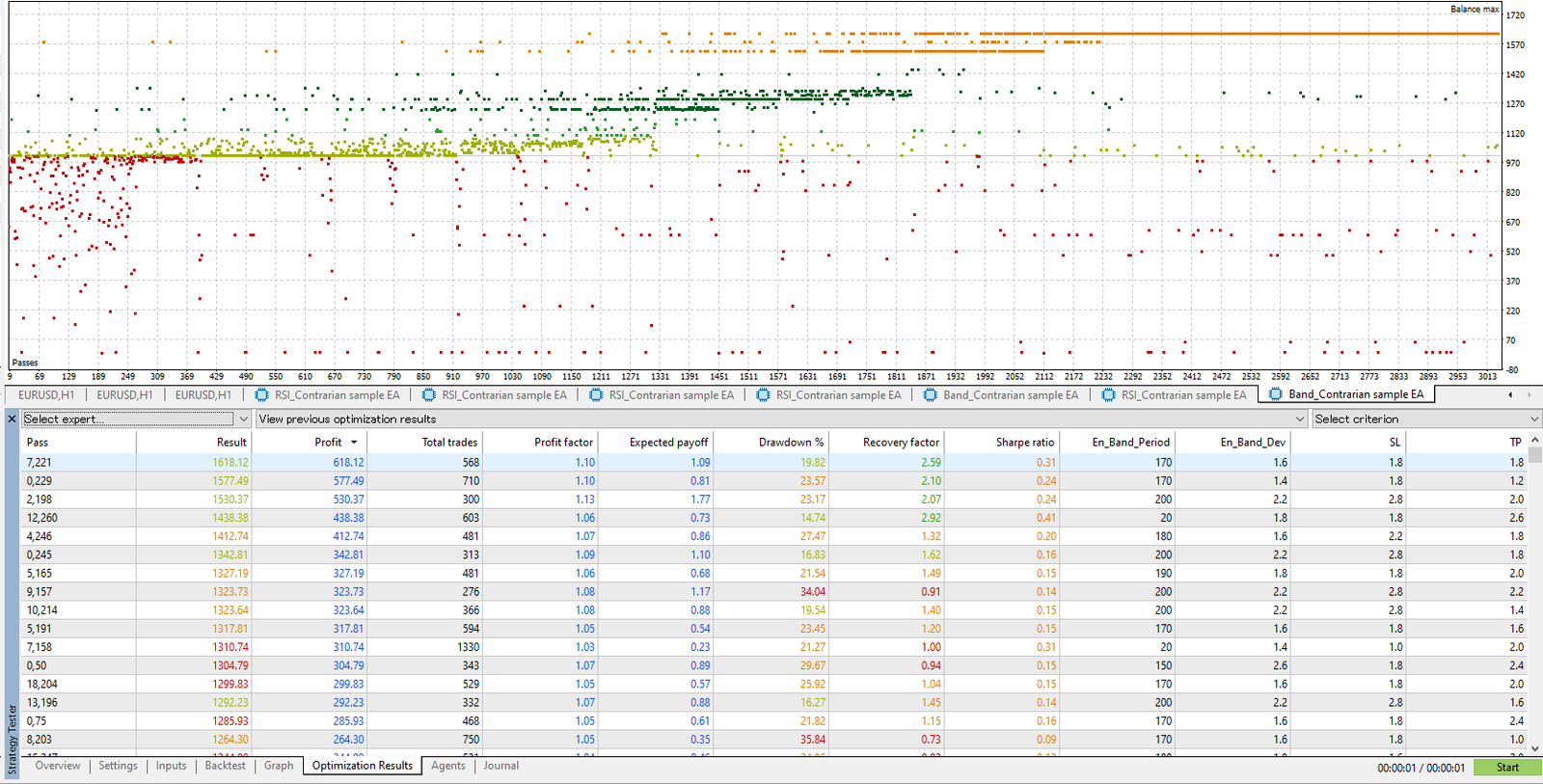

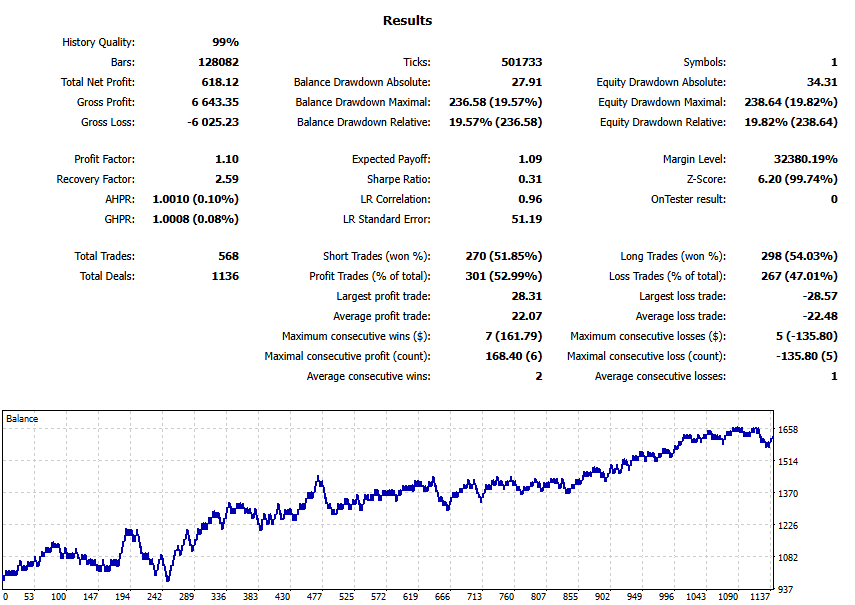

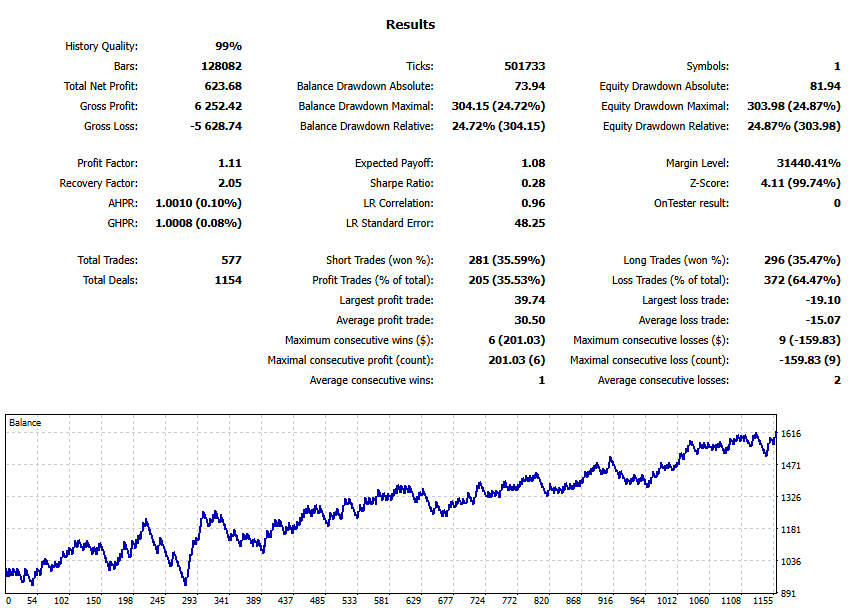

Pattern 1: Bollinger Band Touch (Contrarian Entry)

- Timeframe: H1 / Symbol: EURUSD

- Period: Jan 1, 2005 – Aug 31, 2025

- Lot size: Fixed 0.01 / Initial balance: 1,000 USD

- Entry: Buy on lower band touch / Sell on upper band touch (contrarian)

- Exit: SL/TP only

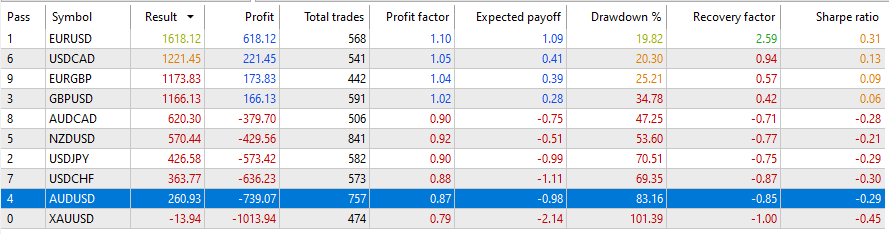

Takeaway: Even with the best optimized settings, a standalone Bollinger Band touch strategy often gets stuck around PF 1.0–1.1. Across long periods and different regimes, it’s hard to maintain a clear edge.

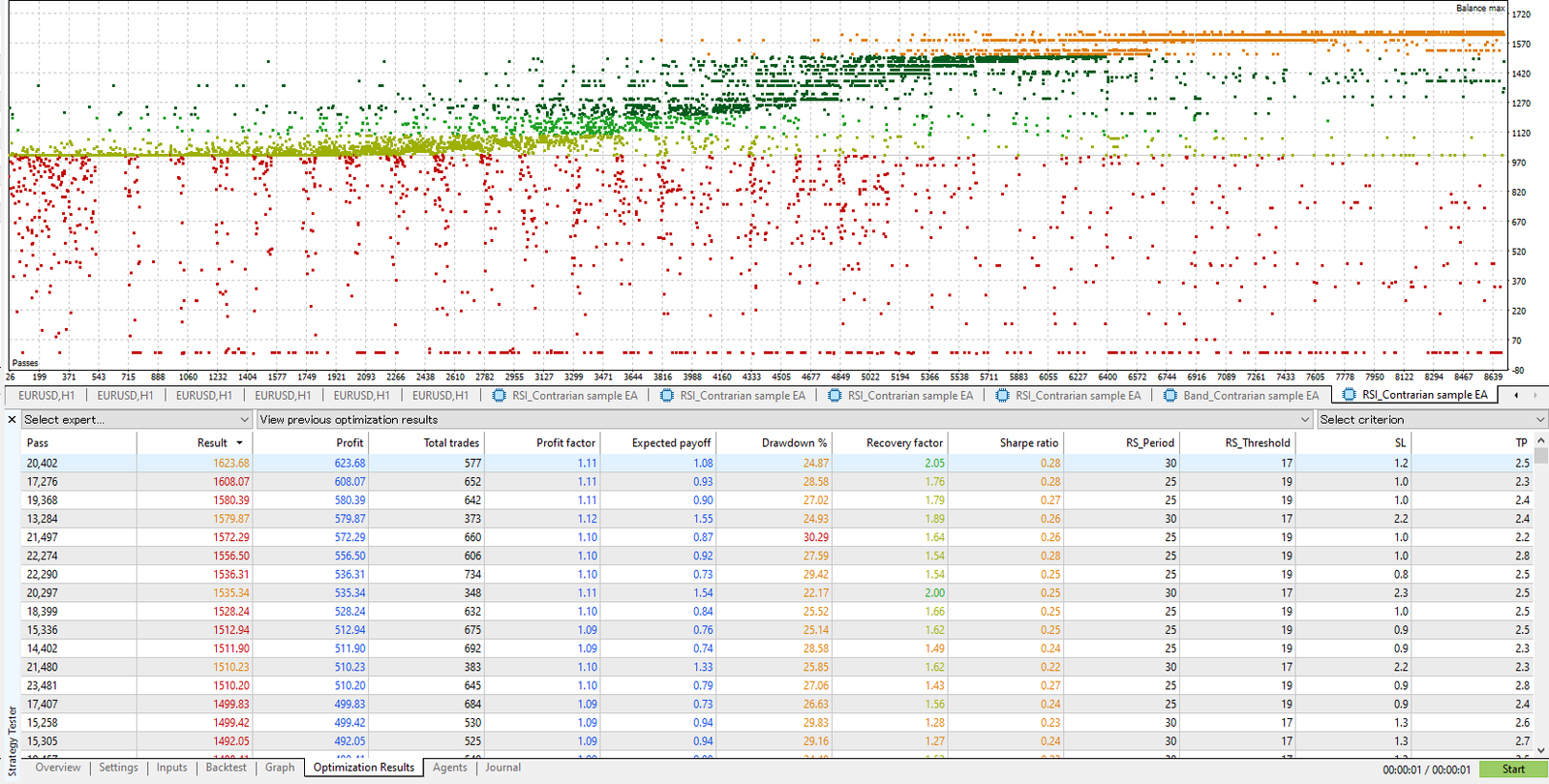

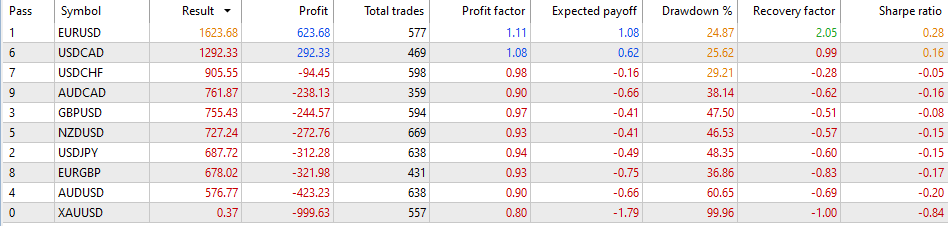

Pattern 2: RSI Break Above/Below a Threshold (Contrarian)

- Timeframe: H1 / Symbol: EURUSD

- Period: Jan 1, 2005 – Aug 31, 2025

- Lot size: Fixed 0.01 / Initial balance: 1,000 USD

- Entry: RSI breaks above threshold → sell / breaks below → buy (contrarian vs. overheating)

- Exit: SL/TP only

Takeaway: A standalone RSI contrarian approach struggles to form a stable “good-performance cluster.” Change the time window and the “best” settings shift dramatically—meaning the risk of overfitting is high.

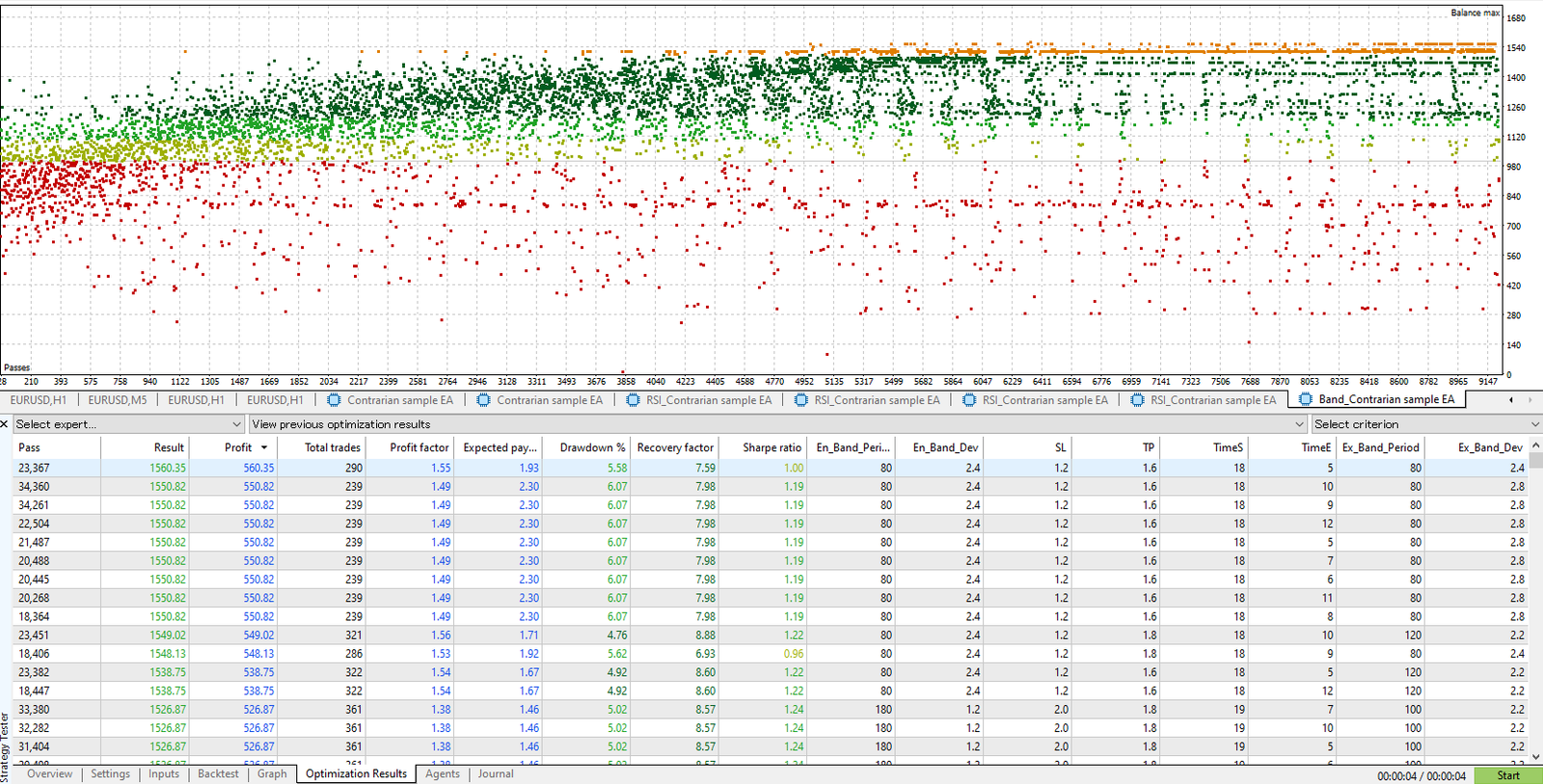

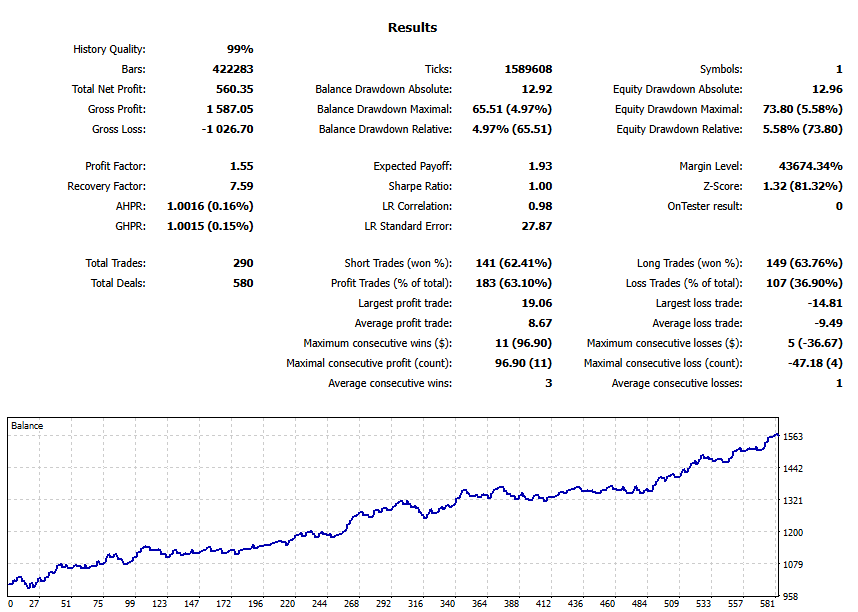

Pattern 3: Short-Term Scalping Test (BB + Exit Logic + Time Filter)

To test a contrarian scalping EA, I used the 5-minute chart (M5) and limited the period to 5 years.

I also added a time filter and exit logic, making the rules more complex.

- Timeframe: M5 / Symbol: EURUSD

- Period: Jan 1, 2020 – Aug 31, 2025

- Entry: Buy on lower band touch / Sell on upper band touch

- Exit: Close when price reaches the opposite band + SL/TP

- Optimization parameters: BB Period/Dev for entry, BB Period/Dev for exit, SL/TP, and time filter (trading hours)

Takeaway: The exit logic and time filter seem to help, but ~300 trades over 5 years on M5 is still a small sample. With limited trades, statistical confidence is not high. You should confirm it doesn’t break across different periods and brokers.

Key Insights from Patterns 1–3

- Contrarian base logic alone has a limited edge. Bollinger Band touches and standalone RSI setups tend to struggle to push PF higher, and optimization results often include plenty of losing regions.

- Adding filters and exit logic can improve results—but the more complex you make it, the more you amplify the risk of overfitting. Don’t judge it by the best optimized window only. Validate reproducibility with forward tests and other checks.

Pros of Contrarian EAs

Strong in Range-Bound Markets

When the market lacks a clear trend, short-term overshoots and reversals tend to repeat. If conditions match, contrarian EAs can create more entry opportunities and more chances to capture profits. The flip side is that they’re generally weak in trending markets.

They Often Show a High Win Rate

In ranges, price “comes back” repeatedly, so when the logic fits, win rate often rises. The more the strategy focuses on small rebounds, the more it can produce an impressive-looking win rate—and sometimes long winning streaks.

But keep in mind: the higher the win rate, the more likely it is that one loss will be large.

Related:Stop Chasing Win Rate: How to Evaluate Forex EAs with Expectancy, Risk-Reward & Drawdown

The Equity Curve Can Look Smooth

Contrarian systems often aim for small profits many times, so in the short run the equity curve can look like a clean upward slope.

However, “smooth” doesn’t mean “safe.” A rare but large adverse move (a no-pullback day) can break the system, so you must test across long periods and multiple regimes.

Cons of Contrarian EAs (Watch the Tail Risk)

Risk-Reward Often Gets Worse

Contrarian strategies often end up as “small wins, big losses,” which hurts risk-reward.

Even if win rate looks high, one big loss can wipe out a pile of gains.

When evaluating, focus less on win rate and more on the balance between average win and average loss, and whether it can stay profitable over the long term.

Related:FX Trading Expectancy (EV) Explained: EAs, Win Rate, Risk-Reward & Money Management

Big Losses in Trends and “No-Pullback Days”

During strong one-way markets—driven by news, policy decisions, central bank remarks, geopolitics, or flash crashes—contrarian systems often lose badly.

The biggest danger is tail risk: rare losses with huge destructive power.

Even if the balance grows steadily most days, a strong trend can expand floating losses and erase accumulated profits in one shot. This pattern is common—don’t ignore it.

Be Careful: Two “Dangerous EA Types” That Often Use Contrarian Logic

These two EA types are frequently built around contrarian ideas. They can look great in the short term, but over the long term performance often deteriorates sharply—so you should be highly cautious before using them.

Grid Trading EAs

This approach places orders at fixed intervals. In many cases, it’s implemented as contrarian + averaging down (often with Martingale). The biggest issue is that it’s basically designed to “hold until it comes back.”

- Why it’s dangerous: If a trend persists, positions can grow like a snowball and margin can deteriorate fast. In a big trending move, the account can get wiped out.

- The equity-curve illusion: Most of the time it looks like high win rate with a smooth upward curve—but a tail event (a rare, huge move) can wipe it out in one hit. Win rate and PF alone won’t reveal this risk.

- What to check: In the trade history, does it keep adding positions step-by-step and then close many positions at once (basket close)? Does it use a fixed SL? Does the developer’s “maximum positions” setting look unreasonably high?

Related:Why Grid Forex EAs Blow Up: Hidden Drawdowns + Red Flags (Self-Made EA Test)

Scalping EAs

Short-term contrarian (scalp-style) EAs target small profits per trade, so they’re highly sensitive to spread, commissions, and slippage.

Even if backtests or demos look good, real accounts can lose expectancy due to costs and execution, and performance can break.

Because execution quality can translate directly into performance, it’s important to evaluate reproducibility in real conditions (differences by broker and trading hours), not just in a test environment.

Related:Scalping EAs: Why They Often Fail on Live Accounts (Costs, Slippage, Execution)

- Why it’s dangerous: Spread, commissions, minimum stop distance, latency, requotes, and slippage can make a strategy that looks great in backtests/demos fail in live trading.

- The optimization trap: It can overfit to tick behavior or specific hours. If broker conditions or account specs change, the edge may disappear.

- What to check: Does it have forward performance across multiple brokers? Has it been tested under tougher assumptions (wider spreads and worse slippage)?

Summary: Avoid EAs that “win most days but occasionally blow up,” or that “only work in backtests and demos.” Don’t judge an EA by a pretty equity curve or win rate alone.

Design Improvements: Filters and Stop Rules

With contrarian EAs, performance often improves less by “adding more wins,” and more by mechanically avoiding the situations where they tend to fail.

That said, adding too many filters increases the risk of overfitting (great in backtests only).

As noted earlier, my view is that contrarian edge is limited by itself. If the base logic is fragile, building a conservative, long-lasting system becomes much harder.

Add a Volatility Filter

When volatility expands and price is likely to run strongly in one direction, stop trading or reduce risk.

Example: Use ATR or Bollinger Band width to detect volatility expansion, and stop trading when it exceeds a threshold—such as ATR entering the top X% of the past N periods.

Add a Time Filter

Liquidity, spreads, and how well contrarian behavior works differ by trading session. Narrowing the trading hours can improve results.

Example: Focus on hours with strong liquidity but clearer price behavior, and avoid thin-liquidity hours when spreads widen.

Avoid News and Major Events

Contrarian EAs often perform poorly around high-impact events. If you can pause trading around key economic releases or major central bank speakers, survival odds can improve.

Optimize Costs and Execution

The shorter the contrarian timeframe, the smaller the profit per trade—and the more fatal the difference in spread, commissions, and slippage becomes.

Choosing a low-cost broker or using a low-latency VPS can improve results.

However, an EA that changes drastically depending on the trading environment is difficult to manage and often lacks reproducibility—so “avoid it altogether” can be the smarter choice.

Set Clear Stop Rules

Rules like a maximum holding time, pausing after a losing streak, daily loss limits, or equity-based risk caps can help avoid a single fatal hit and improve survival odds.

Testing and Operation Tips (Long-Term + Tough Assumptions)

Backtests Should Be “Long-Term + Tough Assumptions”

Testing it yourself is critical.

- Long-term across multiple regimes: Evaluate across crisis/low-vol/high-vol/trend/range conditions. Don’t judge based on just a few good years.

- Use harsher cost assumptions: Include spread widening, commissions, slippage, and swaps. Contrarian systems are often cost-sensitive, so “easy assumptions” are dangerous.

- Check the shape of max drawdown: Look for one-shot drawdowns that spike suddenly.

Always Check Robustness

- Parameter robustness: Does performance fall apart if you change parameters slightly?

- Forward testing: Can it keep performing well on a live account?

- Portability checks: Does it avoid collapsing on other pairs? Does it avoid collapsing under different spreads, commissions, and slippage environments?

Related:EA Robustness Explained: How to Choose a Forex Trading Robot That Won’t Blow Up

Pre-Purchase Checklist (Avoid Costly Mistakes)

You can’t judge an EA by a beautiful equity curve or a “high win rate” alone. You also need to check robustness.

Below is a checklist to help spot fragile designs—especially common in contrarian EAs.

1) Test Credibility

- Is the backtest period long enough? Does it cover multiple regimes (crisis, low vol, high vol, trend/range)? A rough benchmark is ~20 years.

- Are cost assumptions realistic? Does it include spread widening, commissions, slippage, and swaps?

- Robustness: Does performance stay reasonable when you change parameters?

Related:

How to Read MT5 Backtests: Verify EA Risk with Equity DD & Orders/Deals

MT5 EA Trading Costs Explained: Spread, Commission, Slippage & Swap (Backtest vs Live Reality)

2) Forward Testing

- Where it’s published: Is there a live forward track record on Myfxbook, MQL5 Signals, etc.?

- Account type: Is it a real-money account with a reliable broker (demo-only has low reproducibility)? Ideally, also check that it doesn’t break badly on another broker or different account conditions.

Related:How to Read Myfxbook: Spot Risky EAs (Balance vs Equity, Margin Spikes, Trade History)

3) Risk Management Design

- SL/TP: Does it have a clear stop-loss and take-profit? Is the SL excessively larger than the TP, or (worse) is there no SL?

- Position controls: Is there a cap on max simultaneous positions and total lots?

- Dangerous logic: Does it rely on grid, Martingale, or heavy averaging down?

- Overfitting checks: Does performance collapse with small parameter changes? If you optimize it yourself, does the distribution show lots of losing regions?

Related:EA Overfitting (Over-Optimization): How to Detect It Before You Buy

4) Trading Costs and Operating Conditions

- Check the assumptions: Are the required spread/commission, minimum stop distance, execution method, and latency requirements unrealistically strict?

- How scalp-dependent is it? Overly aggressive scalping (a few pips) is highly environment-dependent and often degrades in live trading.

5) How to Read the Metrics

- Win rate: Extremely high win rates (e.g., 85–90%+) can be a warning sign for rare but massive losses.

- Risk-reward (average win / average loss): Is the average win too small compared to the average loss (small wins, big losses)?

Conclusion: Judge Contrarian EAs by “How They Lose,” Not Win Rate

Contrarian EAs often grind out profits in ranging markets. In the short run, they can show high win rates and a clean, rising equity curve.

But their biggest weakness is taking a huge hit when a trend kicks in. Even if performance looks excellent, it can deteriorate rapidly—so you need to stay cautious.

In my backtest experiments with self-built sample EAs, simple contrarian logic tended to get stuck around PF 1.0–1.1, and I confirmed that cross-pair robustness and long-term reproducibility are limited.

Exit logic and time-of-day controls can improve results in certain conditions, but more complexity also means more overfitting risk.

If you’re considering buying or deploying one, don’t get fooled by win rate or the equity curve. Make sure you understand the strategy’s nature and risks, and decide carefully.